Market Minute: Gold Rush to Bust?

The gold market has been on a tear over the past year, driven by inflation fears, geopolitical uncertainty, and outright speculation. This sustained rally has propelled prices higher, but over the last several weeks, a significant development has taken place—fundamentally altering the structure of the gold market.

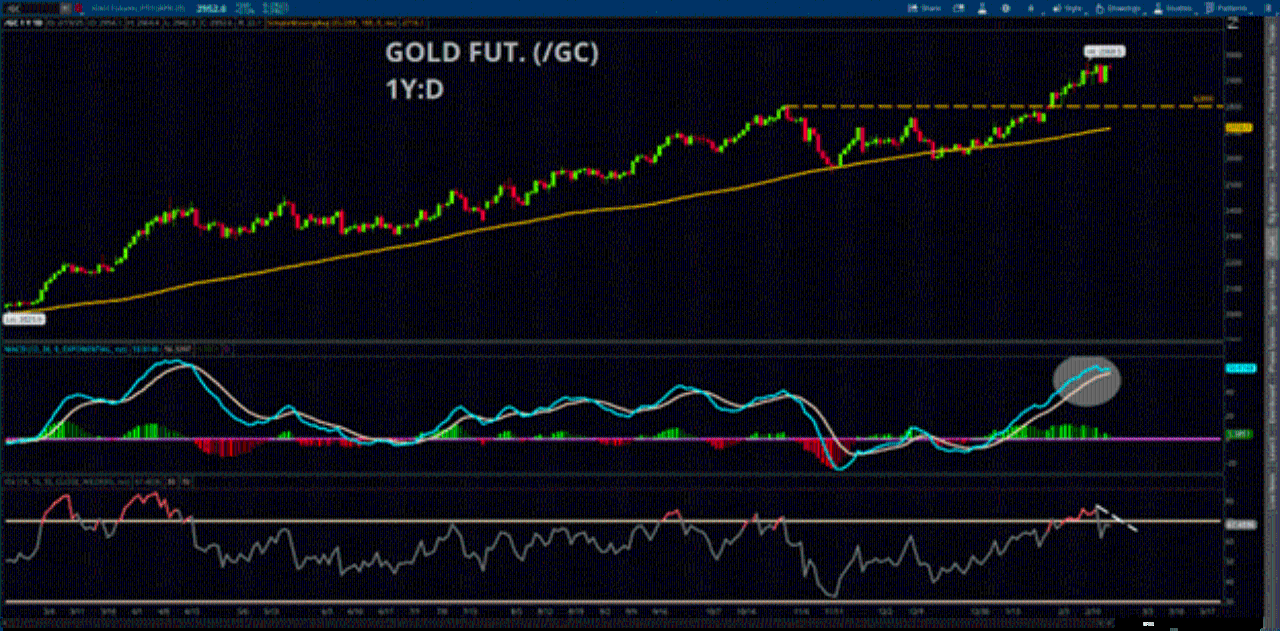

Price is always king, and the current trend remains bullish. However, a key market participant has been rapidly offloading their position with little indication of replenishing their liquidation actions. Today, let’s discuss this gold rush and examine whether we might be nearing peak prices.

Since the start of 2024, gold has surged over 40%, fueled by strong demand—particularly from central banks, with China leading the charge. Economic uncertainty and geopolitical risks have driven these purchases as governments seek to hedge against currency volatility. However, the recent rally in gold, especially throughout 2025, appears to be more structural in nature rather than being driven by fresh buyers entering the market.

A key sign of this shift has been the surge in CME gold futures contracts submitted for intent to deliver which coincides with open interest moving lower as price advances. For context, in futures markets, the seller (the short) has the right to submit an intent to deliver the underlying commodity on or after First-Notice-Day—unlike equity options, where the buyer has the right to exercise the contract, whether it’s a call or a put. Over the past several weeks, the largest gold traders have aggressively submitted orders to deliver physical gold contracts, effectively covering their short positions.

This activity represents a rare kind of short squeeze—one involving the physical commodity itself rather than simply closing short hedge with offsetting with a buy order. The financial institutions submitting these delivery notices are sourcing their gold from overseas, particularly from the London Metals Exchange, as they unwind their hedges. The physical gold is then delivered to customers, with the holdings being stored at COMEX. As a result, these institutions are effectively neutralizing their positions.

In short, these financial institutions were previously long on gold held at the London Metals Exchange. Now, they are taking physical delivery of that gold and unwinding their hedges by submitting intent-to-deliver notices for CME gold contracts. This activity is reflected in the YTD COMEX & NYMEX Metal Delivery Notices.

This repatriation of physical gold has reached such an extreme level that COMEX Gold Warehouse Inventory has returned to near COVID-19 levels. The rate of change in this buildup is also among the most aggressive since the pandemic, making this an outlier in terms of historical trends dating back to 1992.

Over the past three weeks, we have witnessed an unprecedented short-covering event involving physical gold rather than traditional hedge covering. But the key question is: will major gold traders continue this aggressive activity?

If there is no further need to secure additional physical inventory, producers and bona fide hedgers—the market participants typically stabilizing gold trade flows—may significantly reduce their activity. This would leave the market increasingly dominated by Managed Money, which includes:

• Gold ETFs

• Commodity Trading Advisors (CTAs)

• Institutional speculative portfolios

• Financial advisors

• Retail traders

With speculators now controlling a larger share of gold market flows, liquidity could begin to thin and volatility may rise. Historically, when liquidity becomes imbalanced and the market lacks the stability of producers or hedgers, this often signals the end of a trend or the start of a pullback.

This is a crucial factor to watch in the coming weeks. If the gold rush is nearing its peak, we may soon witness a shift in sentiment and a potential reversal in price momentum.

Featured clips

Charles Schwab and all third parties mentioned are separate and unaffiliated, and are not responsible for one another's policies, services or opinions.